1H 2023 Halftime Report

The first half of the year was a welcome reprieve from the carnage of 2022. The Fed is no longer in “crisis mode,” indexes have surged higher, and Wall Street is changing its tune on the possibility of a soft landing.

Add it all up, and this could be the early innings of the next bull market. Although just a label, sentiment matters. Since the lows back in October, the gains from stocks and bonds are bringing optimism back into vogue.

But if this is the next bull market, the playbook from the last one will likely be less effective. Every bull market is different, so it’s time to think fresh and formulate a new approach.

U.S. Economy

The U.S. economy should be in a recession by now. That’s what Wall Street was telling us late last year. The chart below shows they collectively expected 2023 to be the first down year for stocks in decades.

Today, recession forecasts are being pushed back and even dumped altogether. Ed Yardeni, a well-respected and closely followed market analyst, said it best1:

“The permabears will have to postpone their imminent recession yet again based on today's batch of US economic indicators, which suggests that our "rolling recession" is turning into a "rolling expansion.”

How could this be? The Fed just raised interest rates at the fastest pace in four decades. Banks failed just months ago. There’s still a war in Eastern Europe. Big Tech and Wall Street are laying off thousands of well-educated employees. Where’s the growth coming from?

For starters, the housing market appears to be rebounding after a difficult stretch. The chart below shows that 62% of mortgages have a rate below 4%, and 92% have a rate below 6%.

Three years ago, a 30-year mortgage rate was 3.13%, and the median existing home price was $284,000. Today, that same mortgage is 6.67%, and the median price is $396,000. This equates to a $22,000 increase in down payment at 20% and a 109% increase in monthly payment2.

These dynamics have kept homeowners from selling because they can’t afford it. Ironically, this has created a supply crunch that has fueled a recent recovery in homebuilding. U.S. Housing Starts rose by 21% in May, the biggest month-over-month increase since 2016. New home sales also jumped 12.2% from April to May and 20% in the last year3. It’s hard for the broader economy to fall into a recession if the housing market is healthy because housing touches so many sectors.

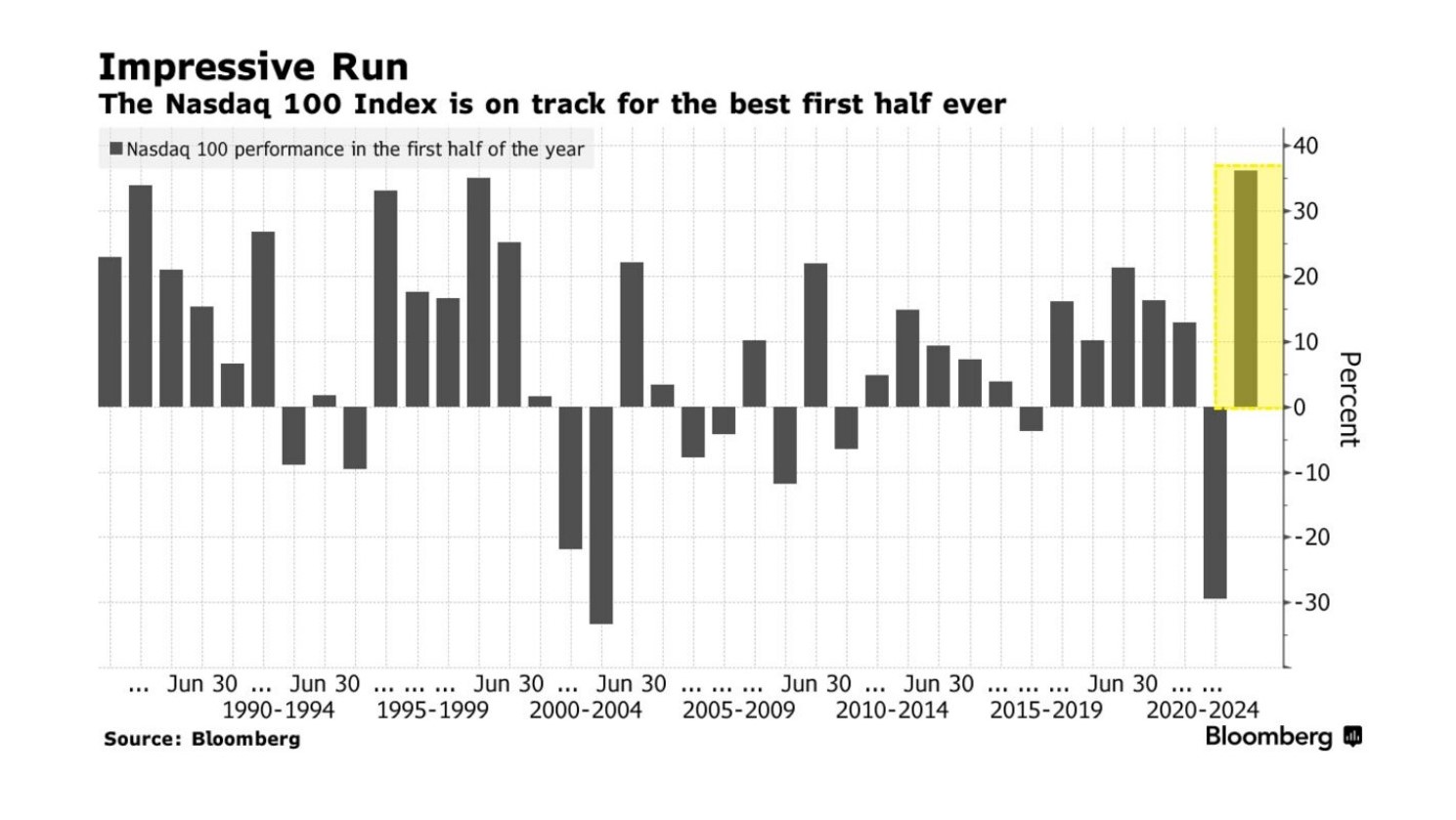

This rally has been a welcome reprieve from one of the worst years on record for stocks. But the evolution of this rally has not been for the faint of heart. It began with just seven technology stocks that today account for over 25% of both indexes. Even more harrowing, the hype surrounding Artificial Intelligence (AI) may have been the catalyst.

But while tech started this bull market, the rally's breadth has since widened. More specifically, sectors tied to the economy's health, like industrials and materials, joined the rally in June. Cyclical groups tend to outperform in the early stages of bull markets.

Fixed income also found its footing after its worst year ever. The total return of the iShares Core US Aggregate Bond ETF is up over 2.5% this year9, and the chart below shows that yields on U.S. Treasury bonds are not only attractive, but some maturities are also beating inflation right now.

Lastly, Bitcoin continued to provide ample drama. On the one hand, two of the largest cryptocurrency exchanges are in the crosshairs of SEC enforcement. On the other hand, BlackRock hopes to get the first spot Bitcoin ETF approved in the U.S. Maybe that’s one of the reasons why it’s thawed from the “crypto winter” and up over 84% this year.

Looking Ahead

Historically, a robust first half in the stock market is a good omen for the rest of the year. According to Ryan Detrick at the Carson Group, since the early 1950s, when the index climbed more than 10% through June, it has risen by a median of 10% in the second half11.

But that’s not to say we can all relax. No matter how much optimism gets injected into financial markets in the second half of the year, there will be pullbacks. Market corrections and drawdowns are features of bull markets, not bugs. So, when they happen, it’s imperative to keep it together.

The real challenge will be getting the playbook right because what worked during the last bull market probably won’t be the best approach this time. Every bull market is different, so our approach for this one will consist of the following.

First, shift more focus to the economy and less on the Fed. Until recently, positive economic data caused the stock market to sell off because it suggested the Fed may raise rates higher. But over the past few weeks, good news no longer appears to be bad news for stocks. When that happens, it tends to be bullish, suggesting the market is looking well beyond the next few months. Hence, we expect economic data to drive our strategies more than what the Fed may or may not do next.

Second, be more careful with valuations going into this bull market than the last one. Valuations didn’t mean much when the Fed kept interest rates at or near zero, but the odds of returning to that monetary policy regime appear low. That means money can’t chase ideas like in the last bull market.

Third, rely more on corporate bonds and Treasuries. Many of these assets used to yield less than inflation, but today, they are often an alternative for investors who don’t want to overweight stocks.

Fourth, get more active in parts of our asset allocation. One reason passive investments did so well during the last bull market was that low interest rates acted as a rising tide that lifted all ships. Now that risk has a price, concepts like intrinsic value and cost of capital could come back into vogue. If so, active managers with an edge may outperform.

Fifth, incorporate investments that may narrow the range of outcomes in a financial plan. New solutions exist today that can often provide protection to a plan without sacrificing as much upside as once was required.

The bottom line is that while there is a lot to be bullish about in the second half of the year, the coast is by no means clear. We will continue to take a measured approach to risk, remain contrarian, and slowly implement this new playbook. Thank you for your continued support.

Sincerely,

Brian Malizia, President

Mike Sorrentino, CFA

Sources

- https://www.yardeniquicktakes.com/the-promised-land/

- https://bilello.blog/2023/the-week-in-charts-6-25-23

- housing

- The Federal Reserve. As of 6/30/2023

- https://www.cnbc.com/2023/06/14/nearly-all-americans-cut-back-on-spending-amid-inflation-cnbc-survey-says.html

- https://www.cnbc.com/2023/06/16/retailers-start-preparing-for-a-deeply-discounted-down-holiday-season.html

- https://www.thestreet.com/retailers/costco-shares-troubling-news-and-one-really-good-thing

- https://www.bls.gov/news.release/jolts.nr0.htm

- Bloomberg. As of 6/28/2023.

- https://www.reuters.com/technology/bitcoin-hits-1-year-high-amid-blackrock-etf-excitement-2023-06-23/

- https://www.bloomberg.com/news/articles/2023-06-25/where-stock-market-is-headed-after-wild-first-half-five-charts

Disclosures

This newsletter/commentary should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions, or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful.