Will This Horror Story Ever End?

The bond market has been in a bear market for longer than any other time in history and seems to be getting worse by the day. Is it time to throw in the towel, or will it find its footing?

The bond market appears to be melting down. If the year were to end today, the Bloomberg U.S. Aggregate Bond Index would be down for three years straight1. That’s never happened before, and while there are several reasons why, let’s focus on three overarching ones before assessing if this turmoil will ever end.

First, the economy has performed better than most investors had expected. Earlier this year, the bond market had priced in interest rate cuts by now due to expectations of an economic slowdown. But the opposite has happened, and the Federal Reserve plans to keep rates higher for longer to tame inflation further. This shift in expectations has hurt existing bond prices due to the “time value of money.”

Let’s say you were offered $1 today or $1 a year from now. The right move is to take the dollar today and invest it for the next 364 days. Assuming you can get 5% interest, then you’ll have $1.05 a year from now. If interest rates rise over the year, you do even better, and that $1 offer a year from now will look worse. That’s essentially what’s happening to bonds right now.

Think of a bond as a series of payments over time. The more payments left in the life of a bond, the more sensitive it is to interest rates because each time rates rise, the value of every future payment falls. For example, Treasury bonds that extend past 20 years have fallen 46% since March 20201. That's the biggest decline on record.

Second, the supply of Treasury bonds that has hit the market recently is unprecedented. The chart below shows that over $2 trillion in new Treasury bonds has been issued since the debt ceiling was suspended four months ago.

The Fed has also reversed course on its bond-buying program known as “Quantitative Easing,” which grew its balance sheet to a peak of almost $9 trillion last year. Today, it’s closer to $8 trillion due to selling some of the bonds they own and letting others mature. Said another way, the largest buyer on the planet for the last decade has stopped buying.

Third, other large buyers like China and Japan have pulled back from Treasuries for various reasons. However, these sovereign nations were not buying Treasuries to make a profit. Instead, they were doing so to enact various policy initiatives, making them “price insensitive.”

For example, China pegs its currency to the U.S. dollar using Treasuries, so they don’t care about the prevailing yield on a Treasury bond when it’s issued. All they care about is maintaining their peg.

Simply put, the Fed and other central banks massively distorted the bond market for years, and now some of this is normalizing.

The bottom line

It’s understandable to want to sell all bonds and wait until things settle down. Why own them with rates rising and the supply and demand imbalance so extreme?

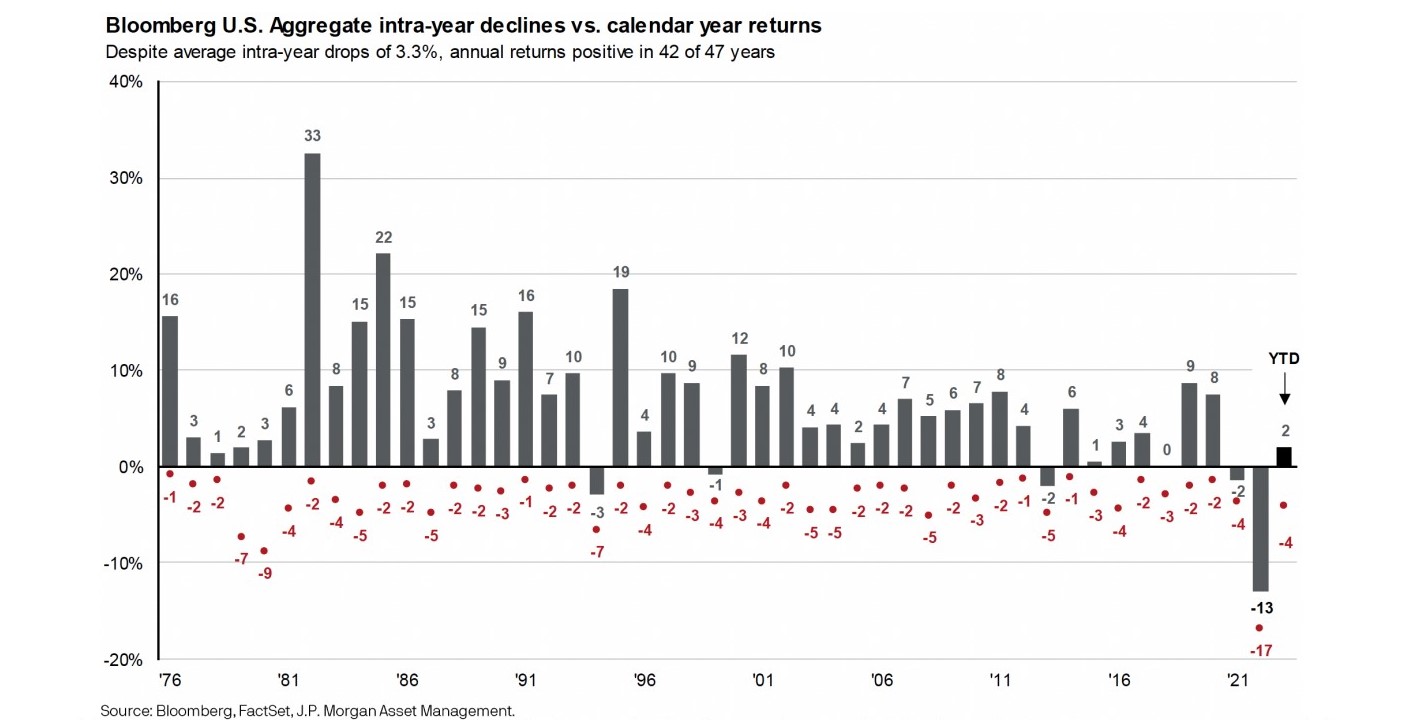

History may argue otherwise. The chart below shows that over the last 47 years, the bond market has ended the year up 42 times (grey bars). Furthermore, bonds experienced a drawdown every single year (red dots). The average intra-year drop has been 3.3%, but larger moves are common.

Furthermore, the table below shows how the bond market has historically responded to the Fed cutting interest rates. Your guess on when the Fed does so is as good as mine, but they will likely at some point. Missing out because of poor timing complicates diversification, and there’s also a good chance of missing out on the early innings of a recovery.

Lastly, even though central banks are buying fewer bonds, no market is ever efficient when governments manipulate them. If this short-term pain is what’s needed to put the bond market back into the hands of rational buyers and sellers, then the ends may justify the means.

The bottom line is that bonds have been in a bear market for a while, but it won’t last. At some point, it will find its footing. Yields will become too attractive to ignore, but trying to time this is impossible and unnecessarily risky.

Sincerely,

Brian Malizia, President

Mike Sorrentino, CFA

Sources

1. Bloomberg. As of 10/12/2023.

Disclosures

This newsletter/commentary should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful.